For the first time that I can remember, I’ve found myself disappointed in the bank that I’ve been a loyal customer of for over 18 years. Longer, if we count Barclays and my BOB Junior account.

I love the service and innovation so much that I’m currently switching the only non-FNB account I have (my bond) away from another bank and bringing it into my FNB portfolio. This account will join my other business accounts, personal accounts, credit cards, debit cards, fuel cards, vehicle finance, insurance, you name it.

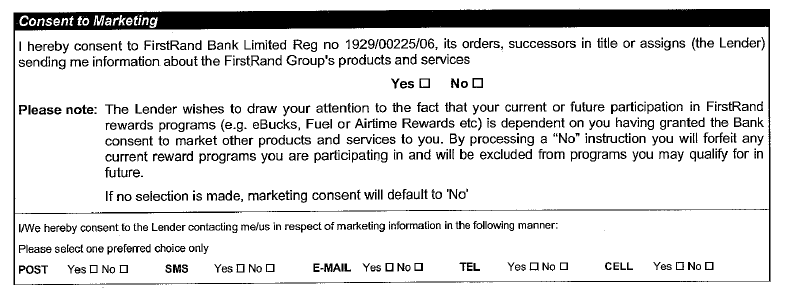

Today I received a document that FNB insisted I sign before the bond switching process can be completed. I’ve included the main content of it below.

The nutshell version is that FNB is instructing me to say YES to receiving marketing of “other products and services”, or “forfeit any current reward programs (I’m) participating in and be excluded from programs (I) may qualify for in the future”. These include eBucks, fuel rewards and airtime rewards.

So hang on. I’m switching my bond account to FNB, adding the biggest asset I own to my existing portfolio that includes my car, credit facilities, call accounts, savings accounts, cheque accounts, cards and other accounts and services, and because I don’t want to receive marketing messages I will be excluded from eBucks and other rewards immediately and in the future? So instead of rewarding me further, I’m being punished for bringing even more business to the bank. Not the ‘do more’ bank I thought I knew.

Does Michael Jordaan (CEO of FNB) know about this? RB Jacobs? Steve from bleep-bank? This is a disservice to the other excellent work FNB does and I’m hoping that this has been created without MJ or RB’s knowledge, and that it will be retracted by the bank immediately – not just for me, but for all other loyal customers too.

I hope to hear from you soon. In the meantime, I’ll still be proud to walk up to the coolest looking ATMs in the country and feel sorry for those who haven’t switched (yet).

UPDATE

As always Michael and RB have been quick to respond on Twitter (kudos to them for taking the time on a Friday night to do so). But rather than leaving me with a sense of security in moving forward, some of their responses have now raised more questions.

Michael responded to this post with: @jasonelk respect your view, would just like to communicate with you. Part of building relationship is communication.

I replied: @MichaelJordaan so my loyalty is only worth rewarding if you can continue to market to me, regardless of my spend? are you going to retract?

And I added: @MichaelJordaan and you should worry less about marketing to me when I’m the one marketing fnb to everyone I know, without reward. now what?

RB Jacobs responded with: @jasonelk Appreciate your view & concerns, I’ll raise this matter with our eBucks team so they can ponder on this. RB

I then replied to both guys: @Rbjacobs @michaeljordaan how about adding extra rewards for saying yes, instead of stopping rewards for saying no?

I added: @MichaelJordaan @Rbjacobs at this point, it makes more sense for me to leave my bond at std bank and still enjoy all my rewards at fnb. yes?

Michael responded with: @jasonelk earning ebucks requires marketing consent, not just for bond. For us comms really NB, we wanna talk to our customers.

He added: @jasonelk idea is to inform you when we think we can add value say switch to email statements, or avoid fees. Not blanket marketing.

I replied: @MichaelJordaan i see this daily in online banking and on social media. just because i don’t want more marketing, i shouldn’t be penalised.

And finally Michael responded: @jasonelk no penalty, eBucks is a reward on top of normal product benefits. Over and out now.

I think my points have been made. Ultimately, I’m being forced to accept as much marketing as FNB can throw at me (there is no limit of any kind included in the document they’re asking customers to sign here), as often as they like, or face forfeiture of “current or future participation in FirstRand rewards programs” including “eBucks, Fuel or Airtime Rewards etc”. That “etc” covers just about anything.

I’m just left deflated by all of this. My business is obviously worth so little to FNB that they’d rather lose me and my accounts than allow me to opt out of receiving marketing. I’ve honestly never seen this kind of our-way-or-the-highway customer communications from any other South African company I’ve dealt with. Unless RB can come up with something, I think it’s time to start thinking about taking my 18 years of banking loyalty elsewhere. It’s not the eBucks or rewards per se, it’s the fact that I’m being told that my business is not worth rewarding unless I completely bend to the corporate wills of a marketing giant that wants to sell me as much as they possibly can, on their own terms, no matter how I feel about the matter.

I wonder how many other FNB customers have felt the same about signing that form, but signed it anyway in fear of being excommunicated from all current and future benefits and rewards.

The ultimate question: Why, if I’m not going to be rewarded, am I moving my bond to FNB? Why am I putting all my eggs in this one non-rewarding basket? Why am I choosing to pay a higher interest rate on my FNB bond than I currently have at another bank, if this is the reception I’m getting when moving over?

The worst part: This should’ve been presented to me upfront, not several months into the process and just 10 days before the switch is about to take place.

The saddest part: I never stop telling people to switch to FNB. I show them how easy the iPhone app is to use. I even ran a fan club for the bank a few years ago. Times have changed I guess – and at FNB in 2012 it appears that, unlike the customers of old, marketing data and conversion targets are now king.

MORE UPDATES

Some more interesting tweets emerged this morning surrounding this issue, all of them supporting my concerns above, with two of the most interesting coming from respected social and digital media lawyer Paul Jacobson:

He commented: @MichaelJordaan if the purpose of the consent is to keep customers informed, the mechanism is too broad

And then added: @MichaelJordaan #FNB is also potentially seeking consent not supported by #POPI as it is arguably coerced

The second tweet raises questions about the legal thinking that went into this document, and I’m hoping that Paul’s comment will give Michael and RB a bit of extra encouragement to properly consider all angles of this issue and revise this document as soon as possible for the benefit of all their customers.

Some other tweets suggested that they also had an issue with signing the document but decided to say YES anyway. They claim that they either (1) have not received any ‘spam’, or (2) simply ignore the marketing they do receive. My issue with (1) is that this document is effectively a lifetime contract with FNB’s marketing department, and gives them the permission to turn on the taps at any time, for any reason, in any amount, for as long as they like. My issue with (2) is that it completely negates the points that Michael Jordaan tried to raise above – if customers are saying YES but just ignoring what they receive, is any of this painful arm-bending even worth it?

EVEN MORE UPDATES

I decided to find out what the Direct Marketing Association of South Africa (DMASA) thought about FNB’s approach to getting customers to opt-in to their marketing messages. The current CEO of DMASA has still not replied to an email but I did hear back from the previous CEO (of 5 years), Brian Mdluli, on Twitter.

I asked him: @BrianMdluli please let me know if this type of marketing behaviour is endorsed by DMASA? who can i speak to? https://jasonelk.com/Fz

He then replied with: @jasonelk the consumer has the right to opt out and no brand can force marketing on any consumer. Basic Marketing provisions in the CPA

I then asked for him for a specific comment on the FNB scenario I’ve described at length above: @BrianMdluli thanks for getting back to me 🙂 is FNB’s withdrawal of earned rewards (if we don’t opt in) acceptable DMASA practice?

And Brian replied with: @jasonelk I cannot speak for the DMA but I would not have endorsed it while I was still head of the DMA. Consent should be free will

Just this morning, lawyer Paul Jacobson has gone on to elaborate on his Twitter commments above, with an extensive blog post examining my concerns and the broader legal and marketing issues FNB is facing here.

I find it interesting that both an experienced legal mind (in Paul Jacobson) and the ex-CEO of DMASA both share my concern in how FNB has approached this issue, while FNB’s CEO sees little problem in doing whatever it takes to ‘talk to the customer’.

FNB, if you really are the ‘do more’ bank your ads claim to be, now would be the time to step in, admit you went too far, and change the execution of your opt-in policies with immediate effect.

ONE MORE UPDATE

MyBroadband‘s business technology news site BusinessTech has provided further coverage of FNB’s one-way-street marketing in an aptly titled article: FNB eBucks: take it or leave it. I’m genuinely surprised that even at this stage, FNB is not changing their position on this matter. I guess at the end of the day, this really goes to prove that while marketing may help to differentiate them, banks are banks are banks.

Until the POPI bill is enacted, and to ensure I’m not losing out on the rewards I’m spending to earn at FNB, I will be ticking the ‘yes’ box on the opt-in form and choosing ‘post’ as my communication option of choice. Mostly because this is the least intrusive of all the methods for me, but partly to prove the point to FNB how ridiculous it is that they’ve now pushed me into say yes to receive printed and posted material that is going to be costing them real money to send me that I don’t want to receive, but that will ironically ‘qualify’ me to continue receiving the rewards I’ve earned. Had this form never transpired, they wouldn’t be spending the extra R10/month (or more) to mail me, I wouldn’t have written this post, and I would’ve still been earning the same rewards I’m continuing to earn as a ‘qualified’ opt-in customer.

This is starting to feel like the Twilight Zone.

I have to add to the disdain you are feeling for FNB.

I made all the effort of switching to FNB which proved to be a massive nightmare. Applied over the phone and they got my name, email and physical address wrong so had to spend 2 hours in the branch sorting it out. Then once my new card was available I spent another 2 hours getting everything sorted including the debit order switching. The consultant at the bank filled everything in, only for me to receive notice a week later that my form was illegible. So I said screw it, and changed them manually.

Now it turns out that in order to use the SLOW Lounge they actually expect you to swipe your card for R5000 every month at retailers. Unless I’m buying an Xbox every month, i don’t see how I can reach that limit. The premier banker actually called me to say I should rather stop paying my bills via EFT and go all the way to the stores to swipe just to reach the R5000 threshold. What a load of rubbish

So it appears that after a whole 6 weeks with the bank, I’m closing my account and going back to the previous bank

Thanks for the comment Arthur. If what you’re saying about the SLOW Lounge is true, it seems that a pattern is starting to emerge of FNB adding all sorts of little fences around their rewards programs and benefits through restrictive terms and conditions. Not a good sign. Hopefully FNB will have the courage and transparency required to reply to your concerns here.

This is an extract of the email I received last Friday (coincidentally the day I wanted to first make use of the SLOW Lounge):

“…and swipes their Platinum Cheque Card at retailers to the value of R5,000 per calendar month – this amount includes swiping your Platinum Cheque Card to withdraw cash at a tillpoint (Cash@Till) as a safer, more convenient alternative to withdrawing cash at an ATM.”

So yeah, what a waste of my time

Jason Elk: “why am I choosing to pay ahigher interest rate on my FNB bond than I currently have at another bank”

Me: “Dude, I don’t know either. That’s pretty stupid.”

All rewards programs have a trade-off. At least it’s just the bank you’re already using getting permission to market to you, not selling your details on (yet).

It’s not a LOT more, and it was after lots of haggling, but really it’s because of the flexible rates and options that come with having your bond together with other accounts at one bank, like transferring between accounts and other such things.

The ‘yet’ in your statement is what worries me on a secondary level. The primary concern is that FNB is changing the rules halfway through the game – a game which I’ve paid to play in, and spent money to be a participant in, and which I shouldn’t be ambushed in as a reward for my participation. Like I said above, they could completely change the tone of the whole thing by making it MORE rewarding instead of less. Anyway, it’s not the end of the world. Just quite disappointing, and even more so with the SLOW lounge news emerging. What else are we likely to find down the road that used to work like X but somewhere along the way changed to work like Y, unless you did Z. Before, it was easy. Spend money on your cards and earn eBucks. No catches. Now the catches are coming, and in the form of very formal far-down-the-line documents. It’s not the way I would’ve handled things had I been involved in the process at the bank – but maybe it’s just me.

I saw this whole thing in the form of banks- and FNB was one of them- contacting existing clients just before the Credit Act came into being. Didn’t I want a WHOLE lot more credit on my credit card and a WHOLE lot more credit on my budget account because I was such a good customer?? Actually– no. I know what I can manage comfortably and I stuck to that.

This is exactly the same thing.They are trying to get one to sign one’s life away before the Act comes through.

Totally agree – and it’s because I’ve always thought as FNB as something different that I was so shocked by their marketing greed here.